Australia’s most read investor-focused magazine for ASX-listed Tech & Biotech stocks

Trending Stories

22 August, 2025

Zip Co’s FY25 Results Mark a Turnaround Built on US Growth and Operational Discipline

Zip Co (ASX: ZIP) has delivered a strong set of full-year results for FY25, underscoring its transformation from a high-growth, capital-intensive fintech into a more balanced and operationally disciplined business. The standout performance came from the US, now the group’s primary growth engine and accounting for more than 70% of transaction volume and over 80% of divisional cash earnings.

Group cash EBTDA surged 147% to $170.3 million, supported by a 30.3% increase in total transaction volume (TTV) to $13.1 billion. Operating margin more than doubled to 15.8%, driven by improvements in both unit economics and credit performance.

Zip’s Chief Executive Officer, Cynthia Scott, characterised the year as a pivotal one for the group. “We achieved several milestones, including delivering over $1 billion in total income and generating more than US$100 million of cash earnings in the US. Disciplined execution and strong unit economics underpinned our performance,” she said.

US Business Drives Performance

The US business led the charge, with TTV increasing 41.6% year-on-year (in USD) to US$6.0 billion—well ahead of the broader market growth for instalment products, estimated at 30–32%. Revenue rose 43.7% in USD terms, reflecting improved customer engagement, increased in-store spend, and growing adoption of Zip’s Pay-in-8 product, which comprised 18% of Q4 TTV.

Customer metrics also improved markedly: active customers rose to 4.3 million, while average spend and transaction frequency per customer increased by 27.6% and 20.3% respectively. Zip also expanded its merchant base in the US and deepened relationships with channel partners such as Google Pay, Chrome Autofill, and Stripe.

Credit performance in the US remained within target, with bad debts held in the 1.5–2.0% range.

ANZ Returns to Growth

In Australia and New Zealand, the company returned to growth with a 5.5% lift in TTV to $3.7 billion. While revenue declined marginally by 0.9%, this was offset by improved portfolio yield, which rose to 19.3%, and an excess spread of 8.7%—up 331 basis points year-on-year. The Zip Plus product continued to gain traction, with receivables up 96% since launch and customer engagement materially higher than Zip Pay.

The ANZ business also launched its Zip Personal Loan in January 2025, further diversifying its product suite. Strategic merchant additions in health, retail and travel verticals supported ongoing customer engagement.

Strengthened Balance Sheet and Capital Management

A key theme in FY25 was the consolidation of Zip’s capital position. The company repaid all corporate debt following a $267 million equity raise in H1 and ended the year with $137.8 million in available liquidity, up from $80.4 million. By July 2025, this had increased to $230.8 million, thanks to additional short-term funding capacity.

Funding initiatives included the refinancing of $2.0 billion in Australian receivables at lower margins and the establishment of a new $400 million five-year warehouse facility. In the US, Zip increased its funding capacity to US$300 million.

An on-market buyback program, launched in April 2025, saw $29.8 million worth of shares repurchased during the year.

Nasdaq Listing Under Consideration

In a move reflecting the company’s increasingly international profile, Zip is considering a dual listing on the Nasdaq while maintaining its primary listing on the ASX. The potential listing is designed to align Zip’s capital markets presence with its growing US operations and rising offshore investor interest, which now accounts for approximately 16% of issued capital. The listing remains subject to board and regulatory approvals.

FY26 Outlook

Zip has issued upgraded guidance for FY26, including:

US TTV growth of over 35% (in USD)

Group revenue margin of approximately 8%

Cash net transaction margin between 3.8% and 4.2%

Operating margin between 16.0% and 19.0%

Cash EBTDA exceeding 1.3% of TTV

While the macroeconomic backdrop—particularly in the US—remains dynamic, Zip appears well-positioned to maintain momentum into FY26, supported by a focused strategy centred on product innovation, credit discipline, and operational leverage.

The business has come a long way from its earlier cash-burning phase, and FY25 represents a significant turning point in Zip’s path to sustained profitability and international relevance.

READ ARTICLE

12 August, 2025

Audeara Strikes China Deal, Expands into Bone Conduction Technology

Hearing technology company Audeara Limited (ASX: AUA) has signed a licensing agreement with Taiwan-listed electronics group Eastech Holding Limited to bring its proprietary hearing personalisation software to the Chinese market, in what it describes as a major milestone in its global expansion plans.

Under the five-year agreement, Eastech’s wholly owned subsidiary, Eastech (Huizhou) Co., Ltd., will integrate Audeara’s technology into medical-grade hearing devices manufactured under Eastech’s National Medical Products Administration (NMPA) certification.

The devices will be sold under a third-party brand via a major Chinese e-commerce hearing aid distributor with national reach across platforms including Tmall, JD.com and Pinduoduo.

Audeara will receive royalties for each unit sold, with no minimum purchase obligations.

China is one of the largest hearing health markets in the world, with an estimated 426.5 million people affected by hearing loss in 2019, a figure expected to grow to 561 million, or 40 per cent of the population, by 2034.

“This agreement aligns technology, regulatory execution and consumer access in a way that accelerates our ability to deliver impact at scale,” Audeara chief executive James Fielding said.

Bone Conduction Partnership

The China deal follows news earlier this month that Audeara has partnered with the Ear Science Institute Australia (ESIA) to develop and evaluate bone conduction hearing solutions for high-need communities.

ESIA will contribute $100,000 and its technical expertise to the project, with Audeara providing product supply and coordination. The program will trial bone conduction devices in classrooms to support children requiring additional listening assistance.

Bone conduction technology delivers sound through vibrations via the skull, bypassing the eardrum and allowing users to hear audio while remaining aware of ambient sounds.

Record Year

The announcements come off the back of record financial results for FY25. Audeara reported cash receipts of $4.9 million, up 38.4 per cent on the previous year, and revenues of $3.786 million, a 21.9 per cent increase.

Growth was driven by the company’s AUA Technology division, which provides hearing personalisation software to third-party audio manufacturers. A follow-up order from US-based cymbal maker Zildjian is expected to materially boost September quarter receipts.

Audeara ended the June quarter with $1.42 million in cash and said it was well-positioned to deliver further growth in FY26 through a combination of international licensing, domestic wholesale expansion and new product innovation.

“This year has been a landmark for Audeara, and we’re entering the next financial year with a clear path to scale both at home and abroad,” Dr Fielding said.

READ ARTICLE

10 August, 2025

Nanoveu’s Triple Play: Chips, Capital, and a U.S. Shopfront

Nanoveu (ASX: NVU) is having something of a ‘moment’, with a trio of announcements in early August signalling an inflection point for the Perth-based purveyor of edge-AI silicon, glasses-free 3D and antimicrobial films.

The week began with news that the company’s long-touted 16nm ECS-DoT chip project is steaming ahead, with fabrication now targeted for Q4 2025 via Taiwan Semiconductor Manufacturing Company’s FinFET process. This isn’t just another me-too processor: it’s aimed squarely at ultra-low-power, AI-on-the-edge applications – think drones, wearables, industrial IoT and defence hardware that can think for itself without gulping power.

The project is being driven by a 24-strong engineering team assembled with the help of the Center for Nanoelectronics and Devices. The talent mix is intentionally layered – PhDs for blue-sky smarts, veterans for the nuts-and-bolts, and juniors to keep the cost curve sensible. On the analogue side, engineers are developing wireless, A/D-D/A converters and power modules for low-energy communications, while the digital team is pushing memory-centric AI architectures and full SoC integration. Packaging is moving to a Ball Grid Array format, which might not thrill the retail investor, but matters deeply when you’re cramming intelligence into a wristband or quadcopter.

If the current 22nm ECS-DoT is any guide, Nanoveu has commercial traction in sight. OEMs in drones and wearables are already evaluating the platform, and early feedback suggests design-wins could precede the 16nm debut.

Hot on the heels of this technical update came the announcement that NVU has begun trading on the U.S. OTCQB under ticker NNVUF. For a microcap trying to gain visibility in the world’s largest tech investment market, this is a low-cost, regulatory-light way to open the shopfront to U.S. investors without the agony of a NASDAQ listing (for now). Managing director Alfred Chong was characteristically upbeat, calling it a “pivotal inflection point” for engaging with U.S. partners and investors.

The timing makes sense. The U.S. capital market is awash with money chasing AI stories, and Nanoveu’s combination of edge AI silicon, glasses-free 3D via EyeFly3D, and the antimicrobial Nanoshield product suite is a cocktail likely to catch a few investor algorithms. The OTC listing allows trading in U.S. dollars during local hours, expands potential liquidity, and gives NVU a platform for possible future uplisting.

Completing the trifecta, NVU confirmed it had wrapped up its strategic $3.02 million capital raising, with the final $400,000 tranche coming from chairman Dr David Pevcic. This final stage had been subject to shareholder approval, granted at the 29 July general meeting. While $3 million doesn’t move needles in the semiconductor world, for a lean ASX tech play it’s a vital shot of fuel – especially given the capital intensity of chip design and packaging.

The sequence of announcements reveals a company moving in lockstep on three fronts: technical execution (chip development), capital markets reach (OTCQB dual listing), and financial underpinning (capital raise). The challenge, as ever for sub-$50 million market cap tech stocks, will be converting engineering milestones and market access into commercial contracts and recurring revenue before the cash runway shortens.

Still, if NVU can parlay its 22nm ECS-DoT wins into volume orders and hit the Q4 2025 fabrication target for the 16nm variant, it will be playing in a field where valuations tend to be dictated by strategic potential rather than trailing earnings. In that context, its recent moves look less like incremental housekeeping and more like deliberate positioning for a larger stage – both in terms of technology and investor audience.

Or, to put it another way, Nanoveu has moved from quietly tinkering in the workshop to wheeling its prototype into the middle of the expo floor – lights on, banners up, and now, thanks to the OTC listing, with a big sign pointing across the Pacific saying “Now open for U.S. business.”

READ ARTICLE

7 August, 2025

xReality Group pulls off Texas two-step with $5.7m deal and $2.1m AI boost

It’s been a week of double-barrelled news for xReality Group (ASX: XRG), the virtual reality training outfit that has one foot in Sydney’s manufacturing floor and the other in the heart of U.S. law enforcement.

On Thursday, the company unveiled its largest-ever order for the flagship Operator XR OP-2 systems — a contract worth up to $5.71 million from the Texas Department of Public Safety (DPS). In the same breath, XRG revealed it had secured a $2.1 million grant from the Australian Government’s Industry Growth Program to fast-track the integration of artificial intelligence into its training systems.

For a company still known to many retail investors for its indoor skydiving heritage, the news cements XRG’s evolution into a serious player in the military and law enforcement simulation space.

A Lone Star order

The Texas DPS, which is responsible for everything from highway patrol to the Texas Rangers, will take delivery of the OP-2 systems in the second quarter of FY26. The contract comprises $4.3 million in software licences, hardware, implementation and two years of support, with a further $1.4 million available for optional services in years three to five.

OP-2 by Operator XR

Given Texas’s size — 30 million residents, sprawling geography, and a law enforcement remit that covers everything from border security to disaster response — the order represents a high-profile endorsement. XRG chief Wayne Jones said the deal “underscores the readiness of our platform for statewide deployment and reinforces our U.S. growth strategy… helping officers train more often, more safely, and with better outcomes for the communities they serve”.

It’s not just about revenue; the Texas DPS is a marquee client in a market of 31 similar agencies across the U.S. — the sort of reference customer that can open doors in procurement-heavy government circles.

Canberra cash for AI push

Closer to home, XRG’s $2.1 million Industry Growth Program grant will be paid quarterly over two years, starting this month. The funds will help ramp up AI integration into Operator XR, enabling real-time feedback, instructor augmentation, and automated scenario creation. The money will also double training weapon manufacturing capacity at the company’s Penrith HQ and fund global security and quality certifications.

Jones said the funding would “fast track Operator XR’s AI roadmap,” building on the recent hire of AI lead Ash Crick, who is tasked with embedding adaptive learning and AI-powered decision support across the platform. The end game is to strengthen XRG’s position as the market leader in tactical simulation for defence and law enforcement.

The bigger picture

These announcements are part of a broader trend where immersive simulation tech is being adopted as a safer, cheaper and more flexible alternative to live training. For XRG, the combination of a high-profile U.S. contract and government-backed R&D funding positions the company to chase larger global defence and law enforcement opportunities.

From a business development perspective, the Texas deal validates XRG’s product in one of the toughest public safety environments in the world, while the Industry Growth Program grant provides a war chest to enhance differentiation and scalability.

As Jones might put it, XRG is now training both sides of the Pacific — and with Texas on board, the company’s next steps could have a distinctly global cadence.

READ ARTICLE

6 August, 2025

Adisyn’s Graphene Gambit: Could This ASX Small Cap Be the One to Displace Copper in the Chip Race?

In the semiconductor world, the smallest connections often carry the biggest implications. For over two decades, copper has been the interconnect material of choice, faithfully carrying electrical signals across ever-smaller chip designs. But as transistors shrink beyond the 5nm threshold and data demands surge, copper is increasingly looking like yesterday’s metal.

This morning, Adisyn (ASX: AI1) entered the next phase of a project that, if successful, could make the industry’s reliance on copper a thing of the past. Through its Israeli-based subsidiary, 2D Generation, the company announced that its low-temperature graphene interconnect program has formally entered Phase One development, backed by a newly commissioned Atomic Layer Deposition (ALD) system in Israel and parallel testing underway at Tel Aviv University.

It’s a highly technical step — but one with global ramifications if proven at scale.

Adisyn’s Beneq TFS 200 ALD system

The Interconnect Problem Nobody Talks About

While chip designers have stretched Moore’s Law to the limits, interconnects — the fine metal lines linking transistors — have become a quiet constraint. Copper, though excellent in bulk, suffers from increased resistance and heat generation at nanoscale widths. This slows signal transmission and consumes more power — neither of which suits the AI-drenched future the sector is heading towards.

Graphene, a one-atom-thick sheet of carbon, offers an enticing alternative. It boasts far superior electrical and thermal conductivity, without copper’s scaling drawbacks. But the catch has always been fabrication. The industry has struggled to grow high-quality graphene films directly onto wafers at temperatures compatible with existing semiconductor processes.

That’s precisely the nut Adisyn is trying to crack.

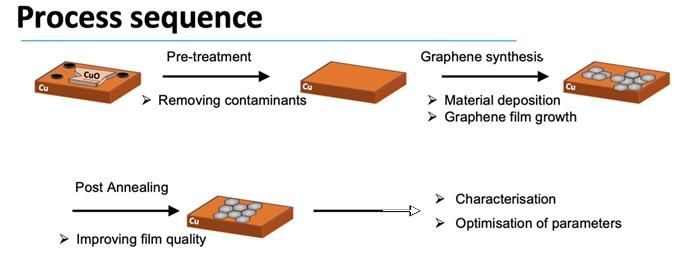

What’s New in Today’s Announcement?

Adisyn’s update confirms the operational readiness of its Beneq TFS 200 ALD system, a platform customised for precision thin-film deposition. The system is now being used to conduct the first phase of graphene growth — a complex, multi-step process designed to validate the company’s proprietary low-temperature deposition method.

The process is more than just laying down atoms. It involves:

Plasma Pre-Clean: Preparing the wafer by removing surface contaminants to allow for uniform film growth.

Deposition Sequence: Reacting selected organic precursors with gases to form initial graphene layers.

Post-Anneal: A thermal treatment that improves the crystalline quality and conductivity of the film.

Characterisation and Feedback: Rigorous testing of each layer to optimise deposition parameters in an iterative loop.

Multiple precursor materials are being trialled through this cycle. If successful, the project will progress to Phase Two in early 2026, focused on wafer-scale integration and commercial collaboration.

Small Cap, Global Ambition

For an ASX microcap, Adisyn is operating in surprisingly elite company. Its R&D efforts are underpinned by partnerships with Tel Aviv University, imec in Belgium — a leading European nanoelectronics research hub — and the EU-backed “Connecting Chips” program, alongside names such as NVIDIA, Applied Materials, and NXP.

The program is led by a heavyweight team, including:

Chairman Kevin Crofton, formerly of Lam Research and SPTS Technologies.

Arye Kohavi, CEO of 2D Generation, best known for founding the atmospheric water company Water-Gen.

Paul Rich, a respected semiconductor technologist with deep expertise in wafer-scale processing and plasma deposition.

Miri Kish Dagan, ex-Tower Semiconductors, who brings decades of advanced materials engineering experience.

Kevin Crofton and Arye Kohavi

Kohavi, not known for understatement, was clear on the significance:

“This is not just about performance — it’s about scalability, sustainability, and what’s possible at the atomic level. If we can validate graphene deposition in a repeatable, cost-effective way, it could become foundational across AI, data, and communications infrastructure.”

Why It Matters to the Sector

If Adisyn’s process works — and that’s still an “if” — the implications could be profound. A scalable, low-temperature graphene interconnect solution would offer foundries a path to continue shrinking chips and boosting performance without a complete retooling of their fab infrastructure.

With Moore’s Law nearing its commercial and physical limits, new materials are no longer optional — they’re essential. Governments, too, are watching. The US CHIPS Act, the EU’s semiconductor sovereignty push, and similar programs in Korea and Japan are all looking for advanced process breakthroughs that can restore or protect competitive advantage.

A validated graphene process, particularly one licensable and fab-compatible, would put Adisyn on the radar of major industry players.

Still Early — But Now It’s Real

To be clear, Adisyn remains early in the journey. The project is pre-revenue, technical risk remains, and wafer-scale reproducibility is a long road from laboratory success. But it’s no longer just a concept on paper. The hardware is installed. The process is running. And the partners are watching.

In a sector where change tends to come from billion-dollar R&D labs in the US, Korea or Taiwan, it’s not often an ASX-listed small cap throws its hat into the ring — let alone with a credible shot at success.

Copper might not be out just yet. But thanks to Adisyn, graphene is no longer just a story of promise. It’s becoming a real competitor.

This article does not constitute financial advice. Readers should seek advice from appropriate advisors before making an investment decision and always do their own research.

READ ARTICLE

Latest News

ALL NEWS

Latest Web & Podcasts

ALL WEB & PODCASTS

Book Now for the Next Edition

Reach real investors through TechInvest Magazine, distributed as an independent insert in The Australian Financial Review, online via www.techinvest.online as well as across investor-focused social media channels.

Book now for TechInvest Edition 4, coming in 2024 with many opportunities to showcase your Tech insights.

What you get:

- Article on your company written by a highly experienced writer or supplied by your company

- Approved article included in TechInvest and replicated on www.techinvest.online

- Two page ‘Company in Focus’ features receive prominent pointer on front page of magazine

- Copy of article (copyright free) for you to use for own marketing purposes

- 10 copies of magazine

Upcoming Webinars

ALL WEBINARS