Australia’s most read investor-focused magazine for ASX-listed Tech & Biotech stocks

Trending Stories

25 May, 2026

PainChek targets US breakout moment with 4DMedical chair appointment

PainChek’s push into the United States has received a significant endorsement with the appointment of 4DMedical chair Lil Bianchi, as the ASX-listed digital health company positions itself as an emerging US healthcare software growth story.

Lil Bianchi

The appointment comes at a pivotal point for PainChek, which recently secured FDA De Novo clearance for its AI-powered pain assessment technology and is now accelerating commercial expansion across North America.

For investors, the parallels with 4DMedical are difficult to ignore.

Bianchi oversaw a period of explosive growth at 4DMedical as the respiratory imaging company transformed from a relatively small ASX healthcare stock into a business now valued at more than $2.5 billion, driven largely by its US expansion strategy. Less than a year ago, 4DMedical was valued closer to $130 million.

PainChek is now attempting to execute a similarly ambitious playbook.

Like 4DMedical, PainChek operates a software-as-a-service healthcare model targeting large-scale adoption in the US market through regulatory approvals, enterprise integrations and reimbursement pathways.

Its technology uses facial recognition AI and observational indicators to assess pain in people unable to reliably self-report, particularly those living with dementia. Delivered through a smartphone or tablet application, the platform is already being used across aged care facilities in Australia, New Zealand, the UK and North America.

PainChek says it has now conducted more than 20 million digital pain assessments globally across more than 2,000 aged care facilities, building what management describes as one of the world’s richest pain assessment datasets.

But the real opportunity lies in the United States.

In a recent investor presentation, chief executive Philip Daffas described North America as the company’s key growth driver and the market expected to take PainChek to profitability.

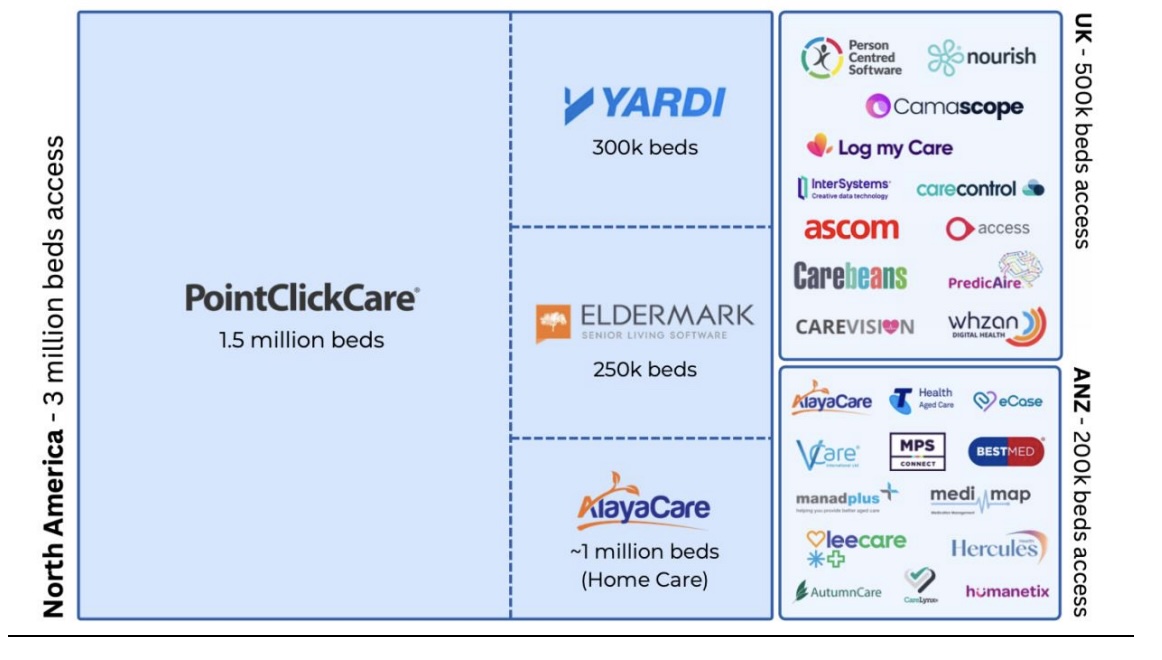

Central to that strategy is PainChek’s integration with PointClickCare, the dominant clinical software platform in the US long-term care sector, which services approximately 1.5 million aged care beds.

The company has already achieved around 35 per cent penetration of the Australian residential aged care market, representing about 70,000 licences.

If PainChek were able to achieve similar penetration across PointClickCare’s US network alone, it would equate to roughly 450,000 beds - before considering the remaining 1.5 million aged care beds across the broader US market.

Importantly, PainChek enters this next phase with established operations already demonstrating commercial traction.

Its Australian business has reached operational break-even, while the UK business has now surpassed 50,000 beds - more than 10 per cent market penetration - and is approaching short-term operational profitability. The UK operation also grew licensed beds by approximately 9 per cent during the March quarter.

That materially changes the investment proposition.

Rather than funding an unproven concept, investors are increasingly looking at a business with validated commercial models in Australia and the UK attempting to scale into the world’s largest aged care market.

Management believes the company is now moving beyond groundwork and into scaled commercial execution.

Last week PainChek secured $5.5 million in convertible note financing to support US sales expansion and working capital, with the company saying the funding would maintain momentum in North America following its “landmark” Sabra agreement.

Sabra Health Care REIT has exposure to more than 20,000 aged care beds across the US market. Under the arrangement, individual facilities can adopt PainChek through a streamlined opt-in process with head office approval, creating what investors hope could become a scalable rollout model across the network.

Management also believes the Sabra agreement could become a blueprint for similar partnerships with other major healthcare REITs and aged care operators across North America.

PainChek has also signed Jewish Home Family, a respected US aged care provider led by Carol Silver Elliott, the former chair of LeadingAge and Jewish Senior Life.

Within the ageing services sector, Elliott is viewed as a highly influential figure, with her support potentially opening broader industry relationships and referral pathways across the US market.

Taken together, PainChek’s North American strategy appears to be forming around three pillars: enterprise software integration through PointClickCare, direct operator penetration via groups such as Sabra and Jewish Home Family, and reimbursement.

Daffas recently told investors the company was pursuing multiple reimbursement pathways tied to its FDA-cleared status, including Remote Therapeutic Monitoring opportunities that could potentially unlock reimbursement claims of up to US$150 per resident per month.

PainChek is also pursuing broader home care opportunities in the US market, which management says could ultimately become significantly larger than the institutional aged care sector.

Bianchi’s appointment signals the board increasingly sees PainChek not simply as an Australian and UK aged care technology company, but as a global healthcare software platform entering its next phase of commercialisation.

“I am absolutely delighted to be appointed Chair of PainChek at this exciting moment in the Company’s journey,” Bianchi said following her appointment. “PainChek is well positioned as the world’s first FDA-cleared medical device for pain assessment.”

Whether PainChek ultimately follows a trajectory similar to 4DMedical may depend on how quickly those US partnerships convert into contracted beds, recurring revenue and scaled adoption across the world’s largest healthcare market.

READ ARTICLE

20 May, 2026

Mach7’s US imaging win puts speed back on the scan

Mach7 Technologies has added a useful new US customer, signing American Radiologist Network Inc, better known as AMRADNET, to a five-year annual subscription licence for its eUnity Viewer. The initial contract value is A$1.7 million, based on a minimum of 675,000 imaging studies a year, with volumes projected to exceed one million studies during the five-year term.

For a company with a market value sitting in the small-cap healthcare tech basket, this is not a company-making deal on its own. But investors are unlikely to view it solely through the dollar figure. The more interesting part is what the contract says about Mach7’s execution, the scalability of eUnity and the company’s attempt to shorten what has historically been a long and lumpy enterprise software sales cycle.

Why AMRADNET matters

AMRADNET is a US-based teleradiology provider whose SaaS-based Radiology Informatics Portal connects US board-certified radiologists with healthcare facilities for remote imaging interpretation and reporting. Its client base has expanded from long-term acute care and skilled nursing institutions into hospitals, outpatient centres, urgent care centres and diagnostic clinics. It is also pushing into cardiology, neurology and broader telemedicine services.

That matters because teleradiology is a volume game. The more studies flowing through a platform, the more important speed, interoperability and reliability become. Mach7’s eUnity Viewer is designed for high-volume diagnostic image access, which makes the AMRADNET win a useful reference point in a US market where remote care and distributed reporting models continue to gain ground.

The deployment rabbit pulled from the hat

The standout metric is not only the A$1.7 million contract value. It is the expected time to first productive use: within 45 days. Mach7 says this is a significant reduction from its typical 12-month deployment timeline, attributing the improvement to the removal of silos and a restructuring of its sales and services teams.

For investors, that is the sort of operational detail worth lingering over. Enterprise imaging software sales can be painfully slow, with procurement, integration, compliance and workflow redesign all conspiring to make revenue conversion feel like watching paint dry in a dark room. A 45-day expected go-live timetable, if repeated elsewhere, could improve revenue visibility, customer onboarding and cash conversion.

Chief executive and managing director Teri Thomas framed the deal as both a customer win and an execution marker, saying AMRADNET was building “a scalable and rapidly growing teleradiology platform” and that the speed from evaluation to first productive use highlighted both AMRADNET’s operational focus and the strength of eUnity in “fast-moving, high-volume imaging environments”.

Recurring revenue, but mind the fine print

The contract is structured as an annual subscription licence, which is positive for investors who prefer repeatable revenue over one-off software sales. However, the released details describe an initial contract value rather than spelling out potential upside mechanics if AMRADNET’s imaging volumes exceed the minimum threshold. So while the projected lift beyond one million studies a year is encouraging, investors should avoid assuming a linear revenue kicker unless Mach7 provides more detail.

Mach7’s broader platform combines a Vendor Neutral Archive, the eUnity Enterprise Diagnostic Viewer and its Flamingo suite of modules, supporting workflow, interoperability and data management across complex healthcare environments. The company says its software is built for interoperability and scalability, while also being aligned with cloud ecosystems including Amazon Web Services.

Market reaction says investors noticed

The key question now is repeatability. One fast deployment is interesting. Several would be evidence. Mach7 has told investors it is changing the way it sells and implements software. AMRADNET gives the company a live test case for that claim in a commercially relevant part of the US healthcare system.

For now, the deal is a tidy contract with a potentially larger message: Mach7 is trying to turn enterprise imaging from a slow-moving hospital IT grind into a more scalable, subscription-led growth story. In small-cap health tech, where promises often travel faster than implementations, shaving deployment time from 12 months to 45 days is the sort of thing that will get investors peering more closely at the scan.

READ ARTICLE

18 May, 2026

Racura clears a key safety hurdle as RC220 moves up the dose ladder

Racura Oncology has passed the first formal safety checkpoint in its CPACS Phase 1 trial, with the Safety Review Committee clearing the company to escalate RC220 to the next planned dose level of 80mg/m². For a clinical-stage biotech, this is not a champagne cork moment on efficacy, but it is a meaningful progression through the part of drug development where the market is mostly asking one question: can patients tolerate the stuff?

The answer so far is encouraging. The first three patients in Cohort 1, all with advanced metastatic solid tumours, received RC220 at 40mg/m². The committee found no treatment-related safety concerns, no dose-limiting toxicities and an acceptable safety profile during the observation period. Racura also says all trial patients remain alive, despite their advanced metastatic disease status at enrolment.

Why the doxorubicin angle matters

The CPACS study is testing RC220 in combination with doxorubicin, a long-used chemotherapy that remains potent but is limited by its well-known potential for heart toxicity. Cohort 1 patients were treated first with RC220 alone, then up to six cycles of RC220 plus doxorubicin at the standard-of-care dose of 60mg/m². That matters because Racura is not merely trying to show RC220 can be layered onto existing therapy without making things worse. The larger commercial idea is that RC220 may deliver both anticancer activity and cardioprotection.

That is a neat proposition, if it holds up. Oncology is full of promising mechanisms that trip over tolerability, combination safety, or the cold mathematics of small patient numbers. But the ability to move to the 80mg/m² cohort keeps the clinical thesis alive and gives Racura more data to work with.

Chief executive and managing director Dr Daniel Tillett called the early safety readout “highly encouraging”, pointing particularly to the absence of dose-limiting toxicities when RC220 was combined with standard-dose doxorubicin.

The protocol tweak adds an extra readout

The next cohort will use an updated trial protocol, with an initial lead-in safety monotherapy cycle of doxorubicin before RC220 is added. The practical effect is that Racura can assess RC220’s potential cardioprotective effect using a blood-based molecular test. Patient screening is underway across Australia, Hong Kong and South Korea, giving the company a multi-region recruitment base rather than relying on a single geography.

For investors, this is the useful bit. The trial is still early, but the updated design potentially makes the data package richer. Safety is the first gate. A signal on cardioprotection, if it emerges, would be a more differentiated claim.

The broader Racura story

Racura describes itself as a Phase 3 clinical-stage biopharmaceutical company. Its lead asset, (E,E)-bisantrene, is a small molecule anticancer agent that the company says acts mainly through G4-DNA and RNA binding, leading to silencing of MYC, a key cancer growth regulator. RC220 is Racura’s proprietary formulation of that asset. The company is pursuing programs in acute myeloid leukaemia, mutant EGFR non-small cell lung cancer and the doxorubicin combination program in solid tumours.

The stock is no longer a tiddler, Racura has a market capitalisation of about $509 million.

What to watch next

The next inflection points are straightforward: whether Cohort 2 recruits smoothly, whether the 80mg/m² dose remains tolerable, and whether the pharmacokinetic and biomarker data strengthen the case for RC220’s role alongside doxorubicin. The patient number is still tiny, so extrapolating too much would be a mug’s game. But in early oncology, the first job is to keep the trial moving without safety alarms.

On that score, Racura has done what it needed to do. The bigger question is whether RC220 can graduate from “safe enough to keep testing” to a therapy with a compelling clinical and commercial reason to exist.

READ ARTICLE

18 May, 2026

Swift TV’s aged-care win gives investors a glimpse of the recurring-revenue prize

Swift TV has taken another step from promise to proof, with the enterprise entertainment and engagement platform provider completing its first four aged-care site rollouts for Australia’s largest aged-care provider and securing a further three sites under the same three-year recurring revenue model.

For a company with a market capitalisation of about $11.25 million, even modest commercial traction matters. This is not BHP discovering another Pilbara. But for a microcap technology stock, converting a master services agreement into commissioned sites and recurring subscription revenue is the stuff investors watch closely.

From rollout risk to revenue

The key point is not simply that Swift has installed its Swift TV platform at four aged-care sites. It is that those sites have moved through installation and commissioning, which is when the company says recurring subscription revenue begins.

That distinction is worth making. Small technology companies are rarely short of pilots, memorandums of understanding and “pathways” to large addressable markets. The harder bit is getting customers live, paid and ready to expand. Swift says the initial rollout under its master services agreement has now been completed across the first four sites, with a further three sites committed by the customer under the existing three-year, per-site model.

That takes the contracted deployment footprint to seven sites, assuming the additional three proceed through commissioning as expected. The dollars were not disclosed, so investors are left without the most important number: revenue per site. Still, the shift to recurring subscription revenue gives the story a more measurable spine than one-off hardware or installation sales.

Why aged care matters

Swift’s flagship product is positioned as an all-in-one connected TV platform for enterprise environments, including mining, oil and gas, aged care and hospitality. In aged care, the pitch is not just Netflix for Nan. The platform is designed to combine entertainment, communication and engagement, while supporting integrations that can improve operational outcomes for facility operators.

That matters because aged-care providers run distributed portfolios, often with standardised procurement needs across many facilities. Win one site and a supplier has a reference case. Win several and the conversation can move from novelty to network-wide utility.

Swift says the customer operates a large national portfolio of sites, leaving scope for further rollout. That is the carrot here. The initial seven sites are meaningful for validation, but the investor question is whether Swift can convert the broader portfolio opportunity into a material recurring revenue base.

Management’s message: repeatability

Chief executive Brian Mangano called the completion of the initial rollout “an important step in the commercialisation of Swift TV” and said it validated the company’s ability to deploy across large, multi-site customer environments.

More importantly for investors, he pointed to the revenue model. “Importantly, we are now transitioning into recurring subscription revenue as sites are commissioned, and the early commitment to additional sites highlights the strength of customer demand and expansion potential within this agreement,” Mangano said.

He added that Swift sees the model as repeatable across its customer base as deployments scale.

That is the nub of the investment case. Swift does not need every aged-care home in Australia to become a cash machine overnight. It needs to demonstrate that once its platform lands inside a portfolio customer, additional sites can be added without reinventing the wheel each time. Repeatability is where software-style economics can start to show, provided gross margins, support costs and customer churn behave themselves.

The questions investors will ask next

There are still gaps. Swift did not disclose contract value, annual recurring revenue per site, expected rollout timing for the additional three sites, gross margins, or whether implementation costs are front-loaded. Without those details, investors cannot yet judge the financial weight of the win.

Nor should the customer’s size obscure execution risk. Large aged-care groups can offer expansion potential, but they can also move slowly, demand customisation and squeeze suppliers on price. Swift will need to show that deployments can be done efficiently and that each new site adds revenue without dragging in too much cost.

For now, the update is a credible commercial marker. It shows a live multi-site deployment, early customer expansion and the beginning of recurring subscription revenue under a three-year model. For a small ASX technology company, that is a more useful development than another glossy strategy deck.

The next test is scale. Seven sites are a start. A broader portfolio rollout would be a story.

READ ARTICLE

12 May, 2026

Fluence lands Texas water win as US industry starts counting every drop

Fluence Corporation has added another US industrial water project to its order book, securing a contract worth about US$3.7 million to design and build a water treatment plant for a prominent manufacturer in Texas. The plant will use ultrafiltration and reverse osmosis technologies and is expected to be installed and fully operational by the end of 2026.

For investors, the dollar value is not company-transforming on its own. But the strategic signal is more interesting. Fluence is pitching itself into the intersection of industrial water security, decentralised treatment and climate-stressed US manufacturing regions. Texas, with its periodic droughts, fast-growing industrial base and pressure on municipal water systems, is a useful proving ground.

The project will treat groundwater from an on-site well for use as cooling tower makeup water. Once complete, the facility is expected to produce up to 1.5 million gallons per day, reducing the customer’s reliance on municipal water supplies. Fluence says the system is designed to achieve more than 90% recovery of feedwater, which matters because industrial customers are not just trying to access water, they are increasingly trying to squeeze more output from every litre available.

Water security becomes an operating issue

Chief executive and managing director Ben Fash framed the contract as part of a broader shift among industrial manufacturers facing water scarcity.

“Industrial manufacturers across Texas and other drought-stricken regions in the US are increasingly confronting the reality that water security could become an operational issue,” Fash said. He added that advanced water treatment could help industry maintain production while supporting broader conservation goals during periods of extreme drought.

That is the nub of the investment case Fluence is trying to sharpen. Water treatment is no longer purely a municipal infrastructure story, nor only an environmental compliance cost. For some industrial users, particularly in water-stressed regions, supply reliability is becoming a production risk. Cooling towers are not glamorous, but if they are short of water, the factory does not run as intended.

Fluence’s pitch is that its quick-to-deploy systems can meet tight quality requirements while helping customers become less dependent on public networks. That decentralised angle is important. Rather than waiting for large civic infrastructure upgrades, industrial users can install dedicated treatment capacity on site.

Industrial growth is the main prize

Fluence says the Texas contract forms part of its growing portfolio of industrial projects in the US. The company describes itself as active in wastewater treatment and reuse, high-strength wastewater treatment, wastewater-to-energy, industrial and drinking water markets, with standardised products including Aspiral, NIROBOX, SUBRE and Nitro. It also offers operations and maintenance support, Build Own Operate structures and other recurring revenue models.

That recurring revenue point is worth watching. One-off equipment contracts can be lumpy, especially for a smaller ASX-listed company. Investors will want to see whether Fluence can turn project wins into a steadier base of service, maintenance or long-term operating revenue. A US$3.7 million plant is welcome. A repeatable platform across multiple industrial customers would be more valuable.

Fash was clearly leaning into that ambition, saying Fluence hopes to provide solutions to “many other industrial customers facing similar challenges in the US and abroad”.

Market context for FLC holders

Fluence remains a small-cap stock, so contract news can loom larger than it would for a bigger industrial.

That size cuts both ways. Smaller contracts can be meaningful for revenue visibility, but execution risk is also magnified. Investors will want to track whether the plant is delivered on schedule, whether margins are attractive, and whether the project leads to follow-on work in Texas or other drought-affected US regions.

The key point is that Fluence is not merely selling a piece of water kit. It is selling operational resilience to manufacturers whose water supply assumptions are becoming less comfortable. If management can convert that theme into a broader pipeline of industrial orders, the Texas win may prove more significant than its headline contract value suggests.

READ ARTICLE

Latest News

ALL NEWS

Latest Web & Podcasts

ALL WEB & PODCASTS

Book Now for the Next Edition

Reach real investors through TechInvest Magazine, distributed as an independent insert in The Australian Financial Review, online via www.techinvest.online as well as across investor-focused social media channels.

Book now for the next TechInvest edition with many opportunities to showcase your Tech insights.

What you get:

- Article on your company written by a highly experienced writer or supplied by your company

- Approved article included in TechInvest and replicated on www.techinvest.online

- Two page ‘Company in Focus’ features receive prominent pointer on front page of magazine

- Copy of article (copyright free) for you to use for own marketing purposes

- 10 copies of magazine

Upcoming Webinars

ALL WEBINARS